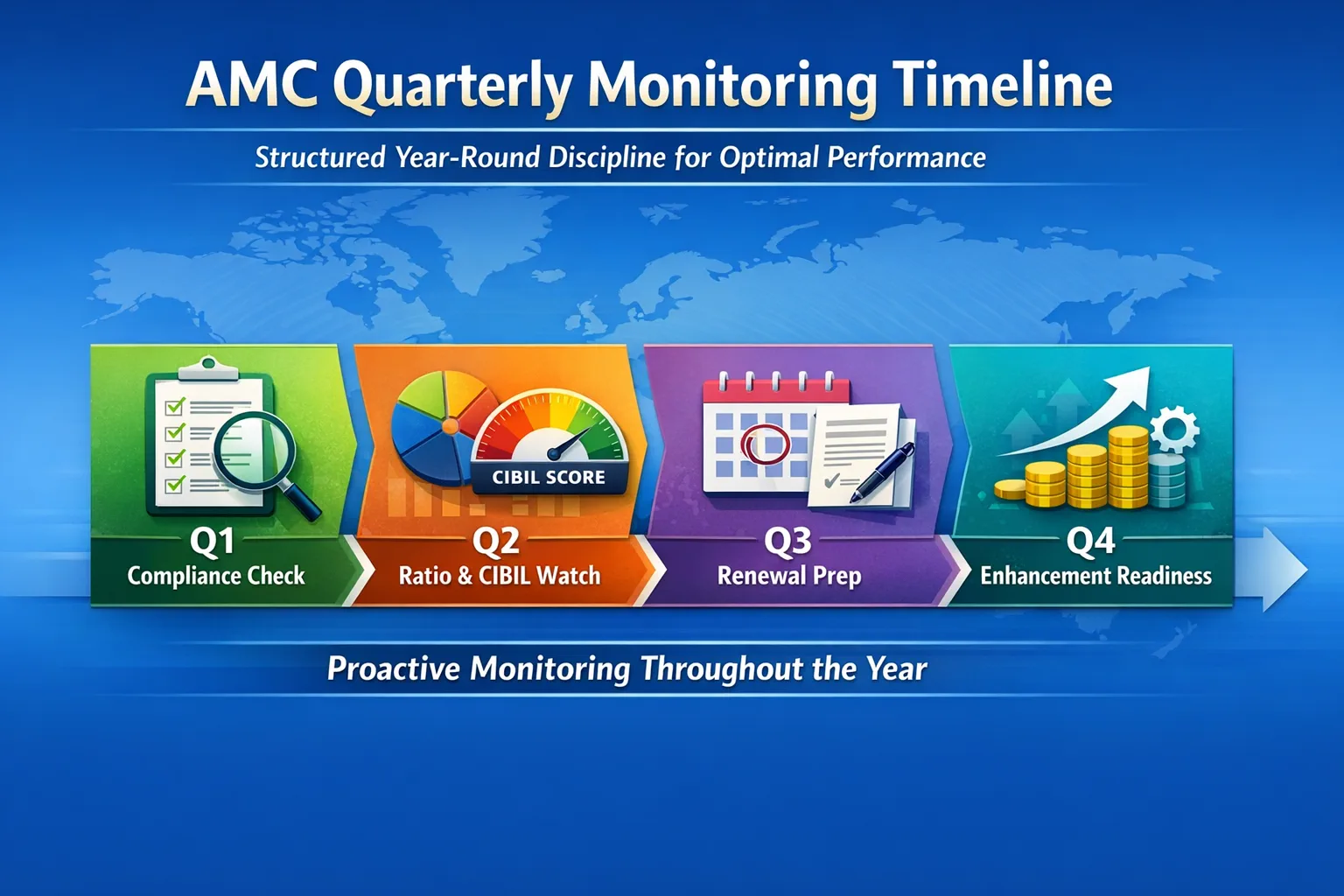

Mistake 1

Letting interest burden outrun operating comfort

Turnover can look healthy while the borrowing structure quietly becomes too expensive for the business to carry comfortably. When interest cost starts to take a large share of operating profit, the banking relationship can begin to feel tighter.

What to do: review whether profits are comfortably covering finance costs, whether the limit size still makes sense, and whether refinancing or better debt structuring is needed before pressure builds.

Mistake 2

Missing month-end interest discipline in CC or OD accounts

Many businesses underestimate how sensitive CC and OD discipline can be around monthly interest servicing. Even short delays can affect the way account regularity is viewed and may create avoidable friction in future banking conversations.

What to do: maintain clear month-end funding discipline, plan inflows in advance, and treat interest servicing as a fixed operational routine rather than something to manage reactively.

Mistake 3

Assuming low utilization means the account is automatically healthy

A lightly used facility is not always a well-managed facility. If monthly interest, charges, or internal monitoring are ignored, the account can still appear irregular or weakly supervised even when drawings are modest.

What to do: monitor account regularity, not just how much of the limit is used. A healthy facility depends on discipline, visibility, and timing - not only on utilization percentage.

Mistake 4

Running too close to sanctioned limits for too long

When a business regularly operates near the edge of its available limit, it can signal stress rather than efficient working-capital use. Persistent edge-of-limit behavior often reduces flexibility and weakens the narrative for future requests.

What to do: track utilization trends, not isolated spikes. If the business is repeatedly running hot, address working-capital planning or enhancement readiness early instead of waiting for the bank to highlight the pattern.

Mistake 5

Keeping a limit structure that no longer matches actual use

Persistent underutilization can be just as revealing as overutilization. It may suggest the business is carrying the wrong limit size, paying for unnecessary headroom, or not reviewing the facility structure with enough discipline.

What to do: compare real working-capital cycles against sanctioned limits, review whether the facility still fits actual usage, and prepare a cleaner banker-facing explanation before the next renewal cycle.