Approval creates access to credit, but the relationship with the bank continues long after the sanction letter. Ongoing discipline often determines how smoothly reviews, discussions, and future requests proceed.

Authority Guide

Why Bank Readiness Matters More Than Most Businesses Realize

Many MSMEs assume the most difficult part of the banking journey is getting a facility sanctioned. In practice, long-term confidence is shaped just as much by what happens after sanction: documentation discipline, responsiveness, periodic statements, renewal preparedness, and the ability to stay bank-ready without panic.

Businesses that can present information cleanly, clearly, and on time are usually easier for lenders to assess. Better structure tends to reduce avoidable friction in the process.

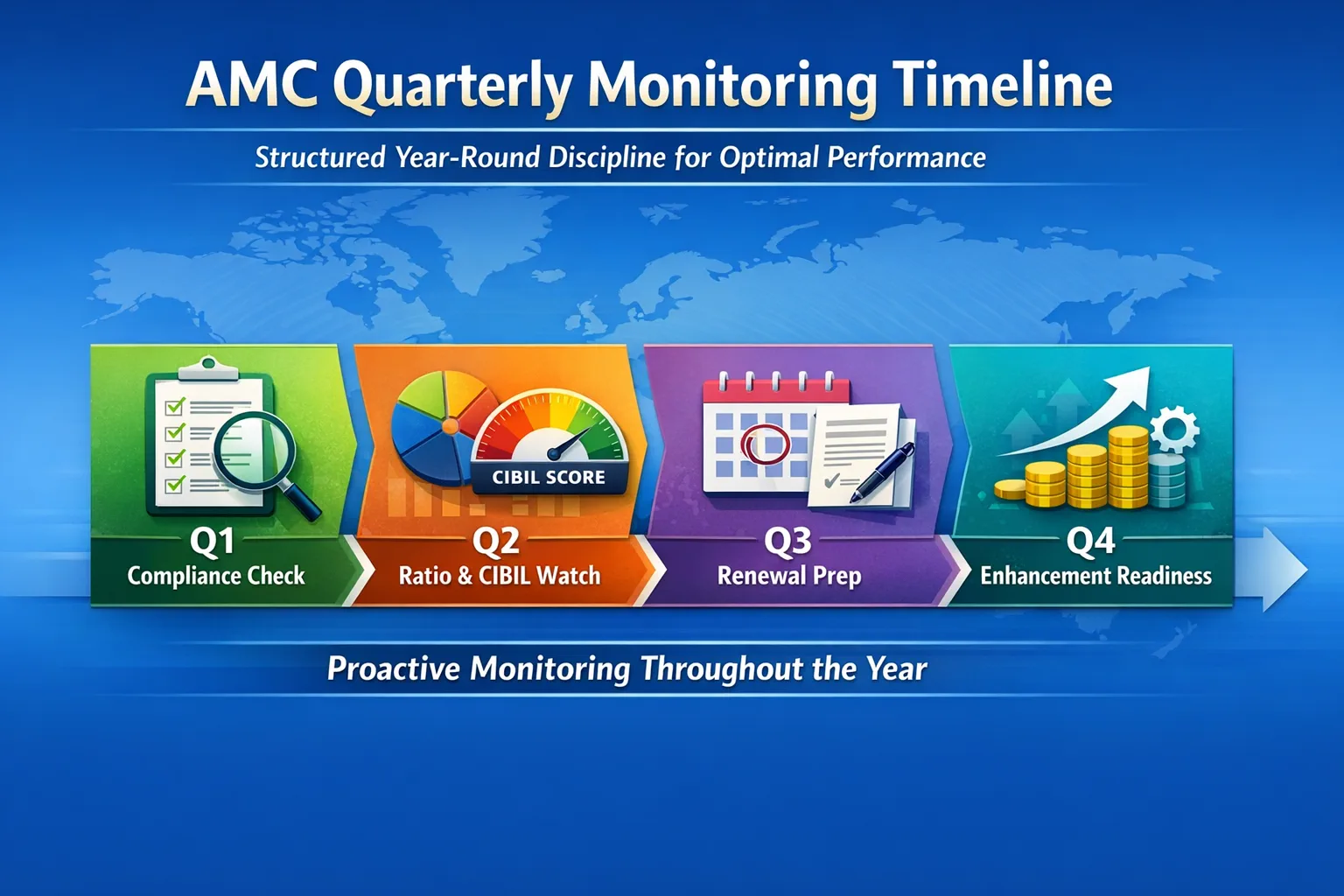

Where recurring stock or book debt statements are relevant, irregularity can create unnecessary pressure. A structured system reduces dependence on last-minute effort.

Renewals are often difficult not because the business is weak, but because preparation starts too late or the necessary data is not assembled in a bank-ready way.

Even when operations are strong, weak visibility on financial ratios can reduce readiness. Better internal awareness supports better planning and stronger banker-facing conversations.

Credit profile issues rarely become easier when discovered late. Earlier visibility creates more room for practical correction and better decision-making.

Growth-related requests are easier to support when the business has a stronger bank-ready narrative, better supporting material, and more orderly presentation discipline.

Businesses often do not need more paperwork; they need a more structured way of managing the paperwork they already have and the responses they will likely need to prepare.

What structured support changes

Preparedness is built through systems, not urgency

When documentation, recurring statements, review cycles, and banker queries are handled as a structured rhythm rather than as isolated emergencies, businesses tend to experience a calmer and more credible banking process.

- Less dependency on last-minute reconstruction of records

- Faster internal coordination with finance, accounts, and CA teams

- Better visibility on upcoming banker-facing requirements

- More confidence in approaching renewals and growth discussions

Related reading

Read our guide on the five discipline gaps that can quietly damage bankability

If this page resonates with your business, the next useful read is our practical breakdown of five common CC, OD, interest-servicing, and limit-structure mistakes that can make MSMEs look weaker to banks than they really are.

Want to improve readiness before pressure builds?

Explore our services, review the optional AMC support model, or start with a free initial review.